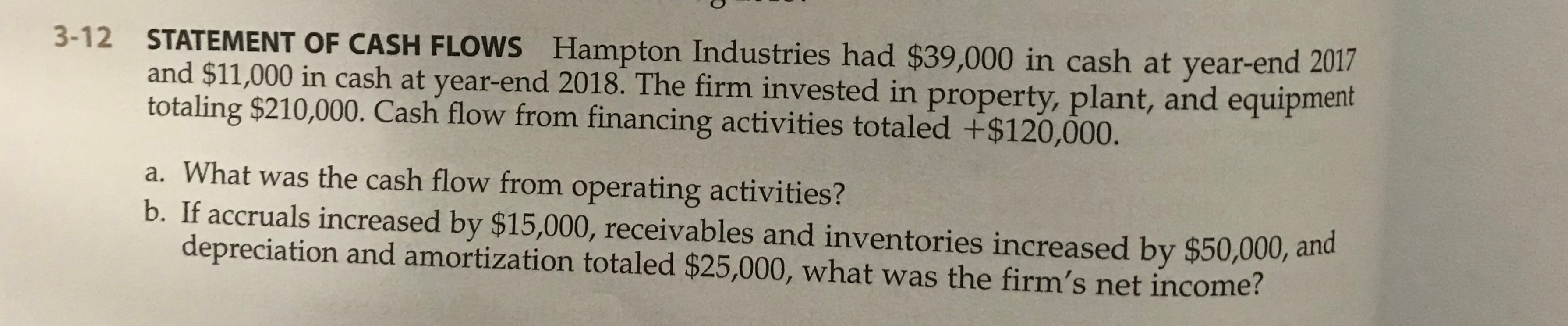

Stop delivering stuck expenses several mortgages when purchasing your following family.

If you are planning to sell your home and get a unique, which ought to you will do basic? If you promote first, you’re going to be under time tension to get a unique domestic easily-and could finish settling for below you desired, overpaying, otherwise needing to blogs oneself and all sorts of your possessions into a hotel room if you don’t can acquire a separate set. But, if you purchase earliest, you are going to need to scramble to sell your dated house-a certain disease if you wish to score a high price on the the new business which will make new deposit into new one.

Possessing a couple home at a time isn’t any dump, both, even when it’s for a short time. You will have to love a few mortgages-on unrealistic enjoy one a loan provider is also willing to give you a home loan for another home in advance of you have sold the initial-plus twice the maintenance, while the security issues that feature leaving one to home empty.

Use the Property Market’s Temperatures

Just before getting your house in the industry or committing to to buy another you to definitely, check out the the prices regarding property regarding areas where you will be both selling and buying. So you can learn how to offer highest and get reduced, needed an authentic thought of how much comparable households was choosing.

And manage whether or not the regional real estate market are “hot” (prefers manufacturers) or “cold” (favors buyers). Once the you happen to be one another a purchaser and you can a seller, you will need to include on your own in your weakened character and work out one particular of your own stronger part.

If market is cooler, you’re in a stronger condition due to the fact a buyer than just like the a good vendor. You may possibly have had your see out of an abundance of properties on the market, at the affordable prices. you possess dilemmas selling yours. To safeguard yourself, you could begin by purchasing an extra home, however ask the vendor while making you buy price contingent up on the offering your existing family. A seller which have a hard time looking a buyer is likely to just accept that it contingency, even though it means in store to find a purchaser. Anticipate to give the vendor plausible reasons why your home will promote rapidly.

In case no provider was willing to accept that it backup, although not, at the least make sure you can be strategy funding. Communicate with a large financial company on what you are able to be eligible for. Next be ready to work easily to put your earliest household on the market after heading to come that have to buy the next one. There is lots you can do beforehand, for example taking good care of maintenance points, going right through documents to the software manuals or any other records you can easily supply the consumer, choosing a real estate agent and perhaps property stager, and so on.

Actions in an excellent Seller’s Real estate market

When you look at the a hot business, selling your home might be convenient than to get another one. To ensure that you dont end up house-faster, you might start with selecting a home in order to pick, following line-up sufficient bucks-utilizing the actions demonstrated less than-so you’re able to tide your more than for the allegedly little while in which you individual two house at the same time.

If you cannot move eg a plan, although not, you could potentially negotiate with your house’s client to have the product sales offer are a supply deciding to make the closure contingent on the shopping for and you may closing to the a new home. Even if couples customers usually commit to an open-finished several months, specific would-be therefore wanting to get your family that they may agree to decrease new closure if you don’t close towards a new family otherwise up until a certain number of days admission, whatever appear very first.

Be also certain to completely check out the industry before you sell, so that you will end up a simple yet effective buyer, who are able to offer the right price for the attractive terms and conditions.

Connection Funding: How to Individual Two House Briefly

What if you will be incapable of very well dovetail brand new sales of a single home with the acquisition of another? You can individual zero home for a while, in which particular case you should have profit the bank and certainly will need a short-term destination to alive. Or you might individual a couple of households at the same time. The following tips should make it easier to deal with instance juggling acts:

If you have nearest and dearest that have adequate free bucks so you’re able to commit, them financing you currency you may suffice each other the welfare and your personal, particularly if you render to pay a competitive interest. Declare that you need assist for a brief period, too. Allow the people putting some mortgage good promissory note, safeguarded by the a moment home loan (action off believe) on your own new house. Make an effort to set it up so no monthly installments are owed until very first family carries. Getting cautioned, but not, one to based the money you owe, institutional mortgage brokers you are going to won’t approve that loan where in actuality the down-payment doesn’t are from your information.

Get a connection mortgage off a financial institution

When you yourself have few other selection, it can be it is possible to to borrow cash out of a bank or most other lender in order to bridge that point between after https://paydayloancolorado.net/boulder/ you intimate towards your new household just in case you have made your finances from the revenue of one’s old one. This concept is you take-out a short-term loan on your existing family, deploying it on the this new advance payment and you can settlement costs on your own new house, and you may paying down they in the event the earliest home sells.

Connection fund can, but not, end up being alot more costly than typical home loan otherwise house collateral financing (higher upfront payments plus rates), plus they are challenging to help you be eligible for. You want enough collateral on the current household and you can sufficient money to spend both mortgage repayments indefinitely. What’s needed all but negate the many benefits of the borrowed funds.